-

-

-

Corporate Style

-

After the National Day holiday, the price of hot-rolled strip steel in China may rise first and then decline

Category: Industry News

Time:2025-09-25

Overview: In 2025. the total supply of hot-rolled strip steel in China will be at a high level, with structural optimization and an increase in high-end demand driving premiums. The price center fluctuated, rebounding first and then falling back in the third quarter

Overview: In 2025. the total supply of hot-rolled strip steel in China will be at a high level, with structural optimization and an increase in high-end demand driving premiums. The price center fluctuated, rebounding first and then falling back in the third quarter, with a year-on-year decline in average price but a slight increase in gross profit. The policy of strengthening science and technology innovation to promote supply optimization, coupled with the resilience of demand in manufacturing industries such as excavators and new energy vehicles, supports the continuation of the pattern of strong competition and weak competition. Mid Autumn Festival and National Day preparations have been launched, and the expected support for the peak season in the fourth quarter may rebound after the holiday, but the sustainability of emotions and the substantial improvement in demand need need to be verified. The following text will analyze the current coiling situation in key areas of strip steel in China and the evolution of pre - and post holiday data over the years.

1、 In terms of price

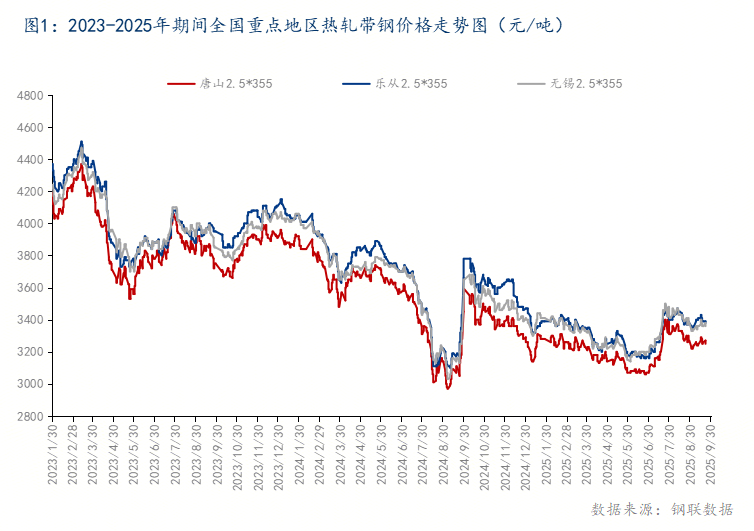

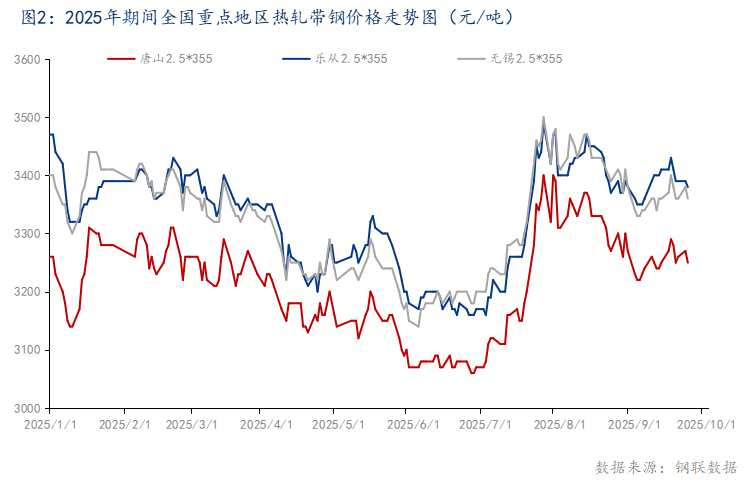

In 2025. the domestic hot-rolled strip steel market will continue to fluctuate and decline for nearly three years, showing a stage characteristic of "first suppression, then rise, and then fall back". The price center will slightly increase year-on-year, and the amplitude will narrow. The core contradiction still focuses on the supply-demand imbalance.

In the first two quarters, prices continued to fluctuate downward due to intensified supply homogenization competition and weak demand in the real estate and manufacturing industries caused by the "general to excellent" transformation. In July, the rebound in iron ore and coke prices drove up costs, coupled with macroeconomic expectations, resulting in a rare rebound of 300-330 yuan/ton in prices. However, due to the lack of substantial increase in terminal demand, the rebound lacked sustainability. In the third quarter, there was a return to oscillation and decline. The settlement average price of North China strip steel in September was reduced by 70-80 yuan/ton compared to August, mainly due to the rebound after the supply decline (the operating rate in Beijing Tianjin Hebei increased to 75%), and the inventory increased by 312000 tons year-on-year. The worsening supply-demand contradiction combined with weak demand during the off-season had an impact.

As of the end of September, the annual price ranges for Tangshan, Lecong, and Wuxi were 3060-3400 yuan/ton, 3160-3490 yuan/ton, and 3140-3500 yuan/ton, respectively, with a range of 330-360 yuan/ton; On September 23rd, prices in the three regions increased by 200-230 yuan/ton year-on-year, reflecting the strengthening role of cost side support, but weak demand still restricts the market from escaping the volatile pattern.

二、供需数据

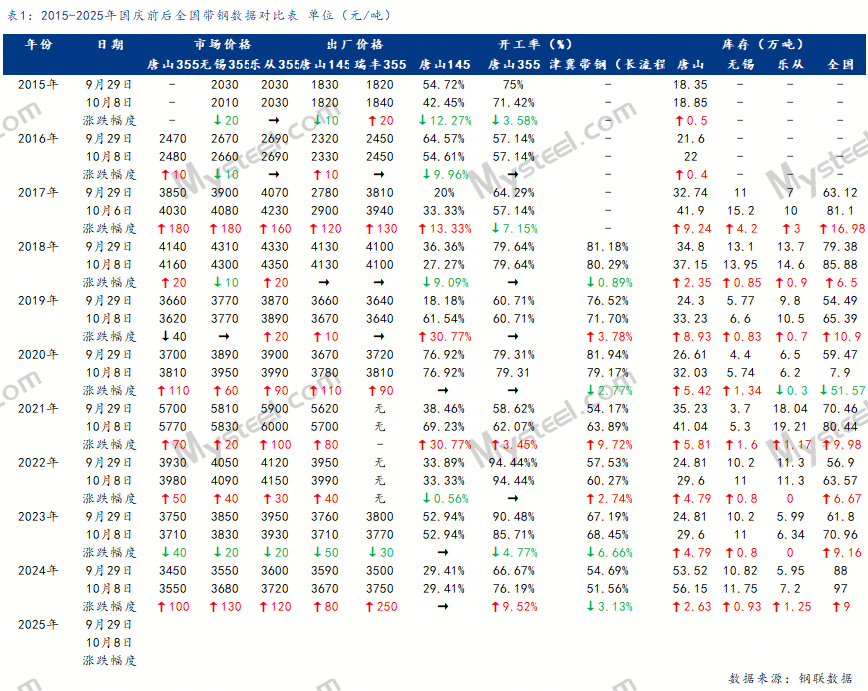

As shown in Table 1 above, the strip steel market before and after the National Day in the past 10 years has shown distinctive cyclical and structural characteristics. At the price level, it rose after the festival in 2015-2019. stabilized in 2019. and some steel mills declined slightly. From 2020 to 2022. it will mainly rise during holidays and after the festival. In 2023. it will fall back year on year due to the impact of macroeconomic and epidemic conditions. In 2024. it will show a trend of "favorable policies before the festival, and adjustment after the festival will fall back". The overall fluctuation is closely related to macroeconomic policies and cost expectations.

On the supply and demand side, the supply side has remained relatively high after the holiday compared to before, with only a slight decrease in monthly capacity utilization rate in 2023. In terms of inventory, there has been a trend of accumulated inventory during the National Day holiday in the past decade, but in recent years, the accumulated inventory has significantly narrowed compared to before, reflecting a more flexible and cautious market inventory adjustment. Prices are generally driven by policies and inventory replenishment in the short term, while in the long term, they are determined by the matching degree between terminal demand (manufacturing, exports, etc.) and supply. After the holiday, prices tend to show a stage characteristic of "fluctuating adjustment" or "first rising and then falling".

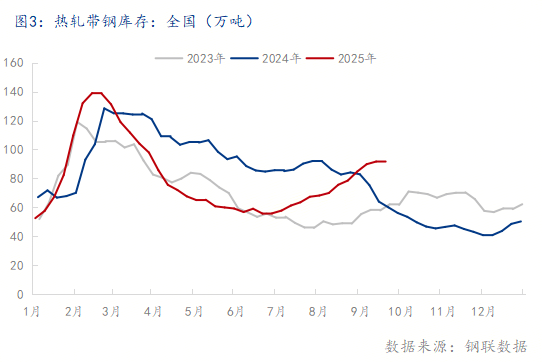

The demand during the peak season of "Golden September and Silver October" in 2025 has become a key variable in price trends. At present, the supply of hot-rolled strip steel industry chain is relatively high, inventory is under pressure, and the table needs to rebound. Although the weekly supply-demand contradiction has slightly eased, the overall situation is still in a state of "strong supply and weak demand".

From a regional perspective, as of the end of September 2025. the social inventory of hot-rolled strip steel in Tangshan has slightly exceeded that of coil steel, and the gross profit of steel mills remains at around 150 yuan/ton. However, the number of orders received has decreased, and inventory may continue to accumulate slightly, with limited incremental growth. The supply in the Northeast region is high, but the amount of resources reaching the market is not high, making it difficult to have a significant rebound after the holiday. In the East China region, the arrival resources are relatively low, and the supply-demand contradiction is not yet obvious. In the South China region, the supply of rolls and tapes is high, and inventory may be under pressure. Overall, there is unlikely to be a significant increase in domestic hot-rolled strip inventory after the holiday, and there may be a slight rebound in demand.

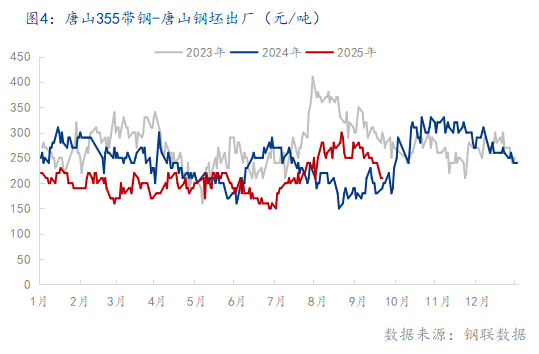

3、 Price difference between billet and strip

As shown in Figure 4. the price difference between steel billets and strip steel will continue to fluctuate at a low level in 2025. only rebounding to over 250 yuan/ton in August, but it will accelerate and narrow again after only one month. At the beginning of 2025. the inventory of winter storage strip steel will accelerate and accumulate to a high point in nearly 4 years. The export situation of steel billets is still acceptable, and prices are supported. In addition, this year, steel mills' profits will be restored, and the supply level will be maintained at a high level. The overall strip steel price is relatively under pressure, and the steel billets will remain strong, with a low price difference between billets and strips. Until July, when steel mills concentrated on reducing production, the price of strip steel accelerated due to the boost of financial attributes, and the price difference between billet and strip steel was repaired in the short term. With the recovery of the supply side, the inventory of strip steel is now higher than the same period last year, and the price difference between billet and strip steel has shrunk again.

As of September 23rd, the difference between the ex factory price of 355mm hot-rolled strip steel and steel billet in Tangshan is 200 yuan/ton. Compared to the same period in 2023. it remained unchanged and narrowed by 50 yuan/ton. Narrowing by 30 yuan/ton compared to the same period in 2022. At present, in the early stage of the National Day holiday, there are downstream replenishment actions, but the scale is limited. At present, the operation of billet blending and steel rolling enterprises is fairly good, and some steel plants have plans to increase the quantity of billet taken away and reduce the supply of tropical steel due to the allocation of variety profits. At present, the operating rate of strip steel is relatively high, and it is expected that the supply of strip steel may be reduced in a small amount with the maintenance of production lines and the allocation of varieties after the savings. The price difference between raw materials and belts is expected to slightly widen after the holiday.

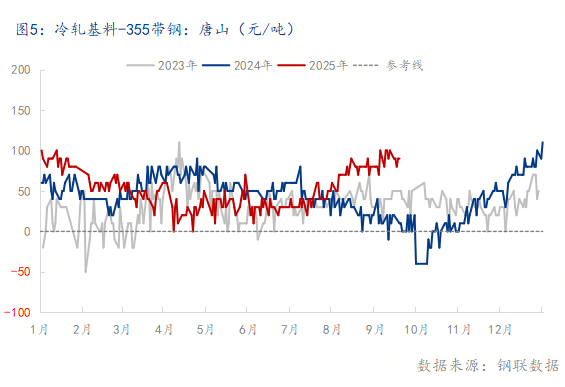

4、 Tape price difference

In 2025. there will be a significant structural differentiation in the price difference of domestic coil and strip related varieties. After the price difference between Tangshan cold-rolled base materials and strip steel decreased, it rebounded to a relatively high level of around 100 yuan/ton. Due to the continuous accumulation of strip steel inventory in the third quarter, which was slightly higher than that of hot coil inventory until late September, the price difference between coil and strip steel will continue to expand; On a national scale, as of September 19th, the price difference of Shanghai's coil belt was -10 yuan/ton (an increase of 100 yuan/ton year-on-year), and the price difference of coil snails was 62 yuan/ton (an increase of 332 yuan/ton year-on-year). The overall industry trend is characterized by strong rolls and weak snails, and the price difference between rolls and belts is expanding.

In the short term, the "strong coil and weak coil" pattern established by the April tariff rush for exports and the rebound in manufacturing demand, driven by the economic cycle, anti internal competition, and unified large market in the new stage, coupled with the start of differentiated inflation cycles in the manufacturing industry, still supports the logic of reshaping the margin of coil and screw differentiation. It is highly likely that the price strength of coil and building materials will continue in the fourth quarter, and iron ore will also maintain relative resistance to decline.

However, we need to be vigilant about the risks on the demand side: building materials have entered the scale verification cycle due to weak new construction data, and may face demand falsification if they rise after the holiday; Although sheet metal relies on the support of the manufacturing industry, there is an objective risk of a downward slope in the growth rate of peak season demand compared to last year, and the intensity of peak season demand may not be as expected. Overall, the market in the fourth quarter will exhibit the characteristic of "the reshaping of the spiral gap continues, but the uncertainty between supply and demand restricts price elasticity". It is necessary to focus on the two-way impact of the substantial increase in manufacturing demand and the verification results of building materials scale on the market.

5、 Summary

During the National Day holiday in 2025. steel companies may continue to maintain a high supply pattern driven by profits, and the release of peak season terminal demand remains to be observed, but the market inventory accumulation space is limited. The core logic of the market in the fourth quarter is the pattern of "maintaining high supply stability, demand verification game, price difference and inventory dynamic adjustment". Although there are expectations of a reduction in exports due to overseas anti-dumping policies, the export increment still has a foundation to maintain in October based on the trade surplus fundamentals. At the price level, in the short term, there may be a slight upward trend in supply structure optimization due to the post holiday stocking cycle and the expected reduction in finished products from steel companies' delivery of steel billets. In the long term, we need to face the pressure of weak real estate and export friction, and the supply-demand contradiction in the industrial chain will once again intensify marginally. In terms of operation, it is recommended that manufacturers focus on inventory dynamics and demand verification, with low inventory and flexible trading as the main focus, and strictly control market volatility risks.

Keywords: After the National Day holiday, the price of hot-rolled strip steel in China may rise first and then decline

Related Information

Company News

-

South Asian imports of scrap steel remain cautious, but Pakistan continues to show buying interest.

Time:2026-05-19

-

Hilton’s “Lightning Meeting”: A Prelude to Collaboration Before the Coffee Has Even Cooled

Time:2026-05-14

-

Warmly celebrate the successful inspection of all sample orders from African customers of Chuangcai Group Co., Ltd.

Time:2026-05-09

-

Chuangcai Group Helps Clients Establish a Strong Footprint in Albania

Time:2026-04-17

-

Warmly celebrate Changcai Company’s successful participation in UzBuild 2026 in Uzbekistan!

Time:2026-02-26

-

Chuangcai’s latest news: Trump puts further pressure on Iran, and coke prices see their first round of increase.

Time:2026-01-29

-

We warmly welcome UAE customers to visit our color-coated and galvanized steel plants.

Time:2026-01-27

-

Warmly celebrate that our Nepalese customer has successfully passed the inspection of all company products.

Time:2026-01-23

-

Chuangcai Group Co., Ltd. launches bright-finish galvanized steel sheets, leading the industry with advanced technology and superior quality.

Time:2026-01-14

-

Warm Celebration of the First Perfect Cooperation between Chuangcai Group Co., Ltd. and Azerbaijani Customers

Time:2025-12-16

-

Warmly celebrate the great success of Chuangcai Group Co., Ltd. at the Dubai exhibition.

Time:2025-12-02

-

Morning reading: The "14th Five-Year" Plan proposal clearly outlines the development direction and opportunities for the steel industry.

Time:2025-10-29

-

Special Meeting on Creative Color Group Corporation's Strategy for Managing Risks in the Indian Market

Time:2025-10-16

-

Warmly celebrate Chuangcai Group Co., Ltd.'s successful participation in Alibaba International's "Heroes Contest, Billion Battle to Fame" high-quality customer negotiation training.

Time:2025-09-15

-

Morning Reading: Iron ore prices rise above $105, first round of coke price reductions implemented

Time:2025-09-09

-

Warmly celebrate Shandong Longjian Board Industry Co., Ltd. for successfully passing the ISO9001 certification

Time:2025-09-05

-

Internal Company International Business Knowledge Collision: Wisdom Integration, Expanding Global Perspectives Together

Time:2025-09-02

-

Two groups of Indian clients visited the factory, securing 3.000 tons of new orders

Time:2025-08-15

-

What industries use galvanized steel sheets? What types are there?

Time:2025-01-08

-

What are the main applications of galvanized materials?

Time:2025-01-08

-

How to distinguish between galvanized sheet and cold-rolled sheet

Time:2025-01-08

-

The difference between galvanized steel sheet and cold-rolled steel sheet

Time:2025-01-08

Industry News

-

If the Strait of Hormuz reopens, Saudi scrap steel prices are expected to fall.

Time:2026-06-18

-

Supported by regional demand, scrap steel prices in the United Arab Emirates rose week-on-week.

Time:2026-06-15

-

With domestic supply tight, why are South Korean steelmakers cutting back on scrap steel imports?

Time:2026-06-12

-

The global billet market is sluggish.

Time:2026-06-08

-

Bureau of International Recycling (BIR): Recycled steel will become the strategic cornerstone of the future steel industry.

Time:2026-06-05

-

Pakistan: Demand recovery remains sluggish following Eid al-Fitr, with scrap trading under continued pressure.

Time:2026-06-04

-

The Brazilian export and U.S. import markets for pig iron remain firm, supported by bullish sentiment among suppliers.

Time:2026-06-02

-

Global scrap steel prices rose by 1–3% in May.

Time:2026-05-28

-

Weak overseas demand has led to a consolidation in Japan’s scrap steel export price range.

Time:2026-05-27

-

Pakistan’s imports of black scrap steel rose 22% year-on-year in the first quarter, reaching 890,000 tonnes.

Time:2026-05-21

-

The International Recycling Bureau highlights the key risks facing the global scrap steel market in the first quarter of 2026.

Time:2026-05-20

-

India’s scrap steel purchases have plummeted, weighed down by shrinking demand for finished steel products, labor shortages, and the depreciation of the rupee.

Time:2026-05-18

-

East Asian scrap steel prices remained steady week-on-week, as the market awaits guidance from the outcome of the Kanto tender.

Time:2026-05-13

-

Global scrap steel prices rose by 10% in April, while European markets remained stable.

Time:2026-05-06

-

Bengal’s demand for imported scrap steel has slowed, with local price advantages suppressing imports.

Time:2026-04-30

-

Democratic Republic of the Congo Establishes Mining Security Force, Allocates $100 Million to Strengthen Supply Chain Security

Time:2026-04-29

-

Brazil Rejects Proposal to Establish a State-Owned Critical Minerals Company, Stalling U.S. Agreement

Time:2026-04-27

-

Pakistan Extends Anti-Dumping Duty on Chinese Steel Billets for Another Five Years at a Rate of 24.04%

Time:2026-04-23

-

Bangladesh Resumes Scrap Steel Purchases from South Korea

Time:2026-04-21

-

Canada’s First Quantum Minerals Partners with Hitachi to Deploy the World’s First Fully Electric Mining Truck at a Zambian Mine

Time:2026-04-20

-

Brazilian Mining Association: Mining Revenue Up 6% Year-on-Year in the First Quarter

Time:2026-04-17

-

2026 Statistics: South Africa’s February Mining Output Up 9.7% Year on Year

Time:2026-04-15

-

Egypt Imposes Safeguard Duty on Imported Steel Billets for a Period of Two and a Half Years

Time:2026-04-14

-

Sea freight rates for iron ore are diverging, with rates on the Pacific route strengthening and those on the Atlantic route weakening.

Time:2026-04-13

-

Ceasefire unlikely to ease Iran’s tight steel supply; semi-finished product prices may remain high.

Time:2026-04-10

-

Ukraine’s iron ore exports fell 33.9% year on year in the first quarter, primarily to China, Slovakia, and Poland.

Time:2026-04-09

-

Increased Chinese Purchases Drive March Global Iron Ore Exports Higher Month-on-Month

Time:2026-04-08

-

Ukrainian Railways’ scrap steel sales surged 220% in the first quarter, poised to set a new annual record.

Time:2026-04-03

-

Australia Bars Hong Kong Investor Yingde from Exercising Voting Rights in Northern Mining, Tightens Controls on Foreign Ownership of Critical Minerals

Time:2026-04-01

-

Uzbek Metallurgical Combine Plans to Procure 300,000 Tons of Iron Ore from Tajikistan

Time:2026-03-31

-

Attacks on Several Core Iranian Steel Mills May Further Heighten Uncertainty in the Middle East Steel Supply Chain

Time:2026-03-30

-

Global scrap steel prices rose across the board in mid-March, led by Turkey and the United States.

Time:2026-03-26

-

February Export Shipments from South Africa’s Saldanha Bay and Richards Bay Decline Month-on-Month for Both Ports

Time:2026-03-25

-

Strong Japanese demand combined with rising costs of alternative raw materials has driven Vietnamese imported scrap steel prices higher for the fourth consecutive week.

Time:2026-03-24

-

Rising freight rates and cautious procurement are putting pressure on the global scrap steel export market.

Time:2026-03-23

-

Vale and Anglo American to Shift Iron Ore Shipments from the Middle East to Asia

Time:2026-03-20

-

Kyrgyzstan Extends Ban on Export of Ferrous Metal Scrap for Another Six Months

Time:2026-03-19

-

Iron ore prices remain volatile at high levels, with Chinese port inventories surpassing 179 million tonnes.

Time:2026-03-18

-

South Asia: Divergent Trends in the Scrap Import Market, with Indian Buyers Becoming More Cautious

Time:2026-03-17

-

Tight supply coupled with the Middle East conflict has driven up freight rates, causing Brazilian slab prices to rise.

Time:2026-03-16

-

The blockade of the Strait of Hormuz is disrupting iron ore trade, forcing cargo ships to seek new destinations.

Time:2026-03-13

-

The situation in the Strait of Hormuz has prompted several iron ore vessels bound for the Middle East to reroute to China.

Time:2026-03-12

-

The export market price for Brazilian billets continues to rise. In February of this year, iron ore exports surged 12.5% year-on-year, with the average price climbing to US$73.4 per tonne.

Time:2026-03-11

-

Energy prices are soaring and freight rates are rising, while iron ore prices continue to climb.

Time:2026-03-10

-

Tensions in the Gulf have driven up the UAE’s domestic scrap steel index, while exports have slowed due to logistical uncertainties.

Time:2026-03-09

-

Soaring freight rates and the Gulf conflict have driven up Bangladesh's scrap steel import prices, while the Baltic Dry Index continues to rise.

Time:2026-03-06

-

Post-holiday restocking in China, coupled with geopolitical risks, has led to a general week-on-week increase in seaborne iron ore freight rates.

Time:2026-03-05

-

The Iran conflict is driving up freight rates, while declining shipment volumes are supporting higher iron ore prices.

Time:2026-03-04

-

Global scrap steel export prices remained stable on a weekly basis, and cautious buying activity continues to keep the market in a volatile pattern.

Time:2026-03-02

-

Japan's scrap steel export market prices remained broadly stable.

Time:2026-02-26

-

Turkey's scrap steel import market prices remain stable.

Time:2026-02-25

-

India and Brazil sign mining agreement; bilateral trade targets over $20 billion within five years.

Time:2026-02-24

-

The South African Mining Council recommends drawing on Finland’s mineral processing model to promote value addition in the mining sector and upgrade industrial structures.

Time:2026-02-13

-

Latest Developments in India’s Iron Scale Market in 2026: Prices Show Strong Momentum

Time:2026-02-12

-

The South African Mining Qualifications Authority will hold a Mining Skills Conference in late February to celebrate its 30th anniversary.

Time:2026-02-11

-

A storm is approaching Australia’s Pilbara region, prompting the closure of liquefied natural gas and iron ore ports.

Time:2026-02-10

-

South Africa and China Sign Framework Agreement on Trade and Investment

Time:2026-02-09

-

China's steel company, Baowu Resources, has acquired a controlling stake in the consortium for the Simandou iron ore project in Guinea.

Time:2026-02-06

-

Import prices for rebar and billets from the UAE remain stable.

Time:2026-02-05

-

Global imports of scrap steel saw a slight rebound, while costs in Turkey rose and pressure on India intensified.

Time:2026-02-04

-

Chuangcai’s Interpretation: The Fed’s Future Policy Direction Still Holds Uncertainty—A Brief Analysis of “Interest Rate Cuts, Balance Sheet Reduction, and a Stable U.S. Dollar”

Time:2026-02-03

-

The global precious metals market plunges; China’s Hubei steel mills conduct winter stockpiling surveys.

Time:2026-02-02

-

Chuangcai Latest News: Supply Increase and Demand Decrease for China's Five Major Steel Products, Chief Outlook on February Steel Prices

Time:2026-01-30

-

China Iron and Steel Association: Production Status of Plate and Strip Products from Key Statistical Enterprises as of December 2025

Time:2026-01-28

-

ChuangCai Consulting: Global crude steel production is projected to reach 1849 million tons in 2025, with a general rise in international commodity prices.

Time:2026-01-26

-

What structural changes will occur in China’s steel demand in 2026?

Time:2026-01-23

-

In the fourth quarter of 2025, Fortescue Metals Group in Australia is expected to produce 49.8 million tons of iron ore, a 2% decrease year-on-year.

Time:2026-01-22

-

This year, the enthusiasm for winter stockpiling of construction steel in Shandong Province, China, has cooled down, and winter inventories will continue to decline.

Time:2026-01-21

-

In 2025, China exported 6,690 ships, a year-on-year increase of 16.2%.

Time:2026-01-19

-

International commodity prices are rising across the board, and several countries are urging their citizens to leave Iran.

Time:2026-01-15

-

China’s latest advisory news: Trump says he’s canceling all talks with Iranian officials; steel futures rise in overnight trading.

Time:2026-01-14

-

China Shagang’s scrap steel prices rise by 50 yuan; China Ansteel, Bensteel, and Linggang announce February price adjustments.

Time:2026-01-13

-

The State Council executive meeting deploys policies to boost domestic demand; Zhongtian Steel and Yonggang announce their latest price adjustments.

Time:2026-01-12

-

Pressure Eases, Resilience Remains—A Forecast of the Impact of Global Steel Trade Remedies on China in 2026

Time:2026-01-09

-

Steel has it all wrapped up at the Northeastern University EXP Building in Boston

Time:2026-01-08

-

Steel-Based Zero Energy Building (ZEB) Inaugurated in India

Time:2026-01-07

-

International bulk commodities generally surged, while black commodity futures fell during the night session.

Time:2026-01-06

-

As the price pattern shifts to a narrowing “W” formation and regional coordination strengthens, can the 2026 stainless steel market maintain steady progress?

Time:2026-01-06

-

January cold-rolled prices may trend weaker.

Time:2026-01-06

-

January Steel Market—Pre-Holiday Weak Realities Weigh Down Prices; Black-Steel Sector Awaits “Spring Surge”

Time:2025-12-29

-

Interpreting the Guidance of Import Coal Price Spreads on Domestic Coking Coal Price Volatility (Part 1)

Time:2025-12-29

-

2026 Steel Market Winter Stockpiling Outlook

Time:2025-12-25

-

The countdown for export licenses has begun! Can China’s galvanized sheet exports reach new highs again in 2026?

Time:2025-12-25

-

Li Qiang called for planning a batch of major projects and undertakings that can drive the overall situation.

Time:2025-12-23

-

Value Equilibrium—A 2026 Outlook for China’s Steel Market

Time:2025-12-22

-

The Ministry of Commerce responds to the management of steel export licenses, and Jiangsu’s winter stockpiling of scrap steel shrinks in scale.

Time:2025-12-20

-

2026 Steel Indirect Export Forecast

Time:2025-12-18

-

Analysis of the Impact of Implementing Export License Management for Seamless Pipe Products and Enterprises’ Response Strategies

Time:2025-12-18

-

Luo Tiejun calls for jointly breaking the cycle of involutionary competition; the chief analyst of sheet and strip forecasts January steel prices.

Time:2025-12-16

-

Multiple ministries are promoting measures to combat “involution”; interpretation of the management of steel export licenses.

Time:2025-12-16

-

The Federal Reserve cut interest rates by 25 basis points, while Zhongtian rebar prices were raised by 50 yuan.

Time:2025-12-11

-

During the 14th Five-Year Plan, China’s steel industry is exploring a path toward reducing output while improving quality.

Time:2025-12-11

-

Multiple regions have activated emergency responses for severe pollution, and the scale of maintenance at steel mills has expanded.

Time:2025-12-11

-

Summary of the Jiangsu Steel Industry Chain Access White List; Shortage of Building Materials Specifications in Yunnan and Guizhou

Time:2025-12-03

-

Steel mills are expanding the scale of production cuts and maintenance, and steel billets in Tangshan rose over the weekend.

Time:2025-12-01

-

The NDRC is promoting measures to address disorderly price competition; this week, steel supply has increased while demand has declined.

Time:2025-12-01

-

Iron ore prices surged above $105, and the yuan-to-dollar exchange rate hit a more than one-year high.

Time:2025-11-27

-

Xi Jinping Holds Telephone Conversation with Trump; International Commodity Prices Rise

Time:2025-11-27

-

Several Federal Reserve officials signaled potential interest rate cuts, while Shagang's scrap steel prices were lowered.

Time:2025-11-24

-

Black futures fell in the night session, with electric furnace steel mills posting a loss of 117 yuan per ton.

Time:2025-11-20

-

International commodity prices fell across the board, while five steel mills raised their prices.

Time:2025-11-18

-

More construction material steel plants have resumed production, and inspection teams will gradually begin operations in the Beijing-Tianjin-Hebei region.

Time:2025-11-17

-

Black futures fell during the night trading session, as the Simandou iron ore project will gradually ramp up its production capacity.

Time:2025-11-13

-

Xinjiang steel plants reduce production during winter maintenance, while the U.S. temporarily suspends its export control rules on penetrating technologies.

Time:2025-11-12

-

In December, Baowu Steel raised prices amid a general rise in international commodity markets.

Time:2025-11-12

-

Supply and demand for the five major steel products both declined, with electric furnaces incurring a loss of 167 yuan per ton of steel.

Time:2025-11-07

-

Steel prices remained stable overall, while coking coal futures rose by more than 1%.

Time:2025-11-06

-

The Drivers Behind China's High Growth in Steel Exports and the Resulting Structural Changes

Time:2025-11-05

-

Morning Reading: 84 New Enterprises Proposed for Entry into Scrap Steel Processing, Baosteel Adjusts Production Capacity Goals

Time:2025-11-04

-

Morning Reading: The Ministry of Commerce Highlights the Consensus Reached in China-U.S. Economic and Trade Talks, While 6 Steel Mills Raise Prices

Time:2025-10-31

-

Morning Read: China-U.S. Leaders to Hold Meeting, Fed Cuts Interest Rate by 25 Basis Points

Time:2025-10-30

-

Morning Read: "One Line, One Bureau, One Meeting" Makes a Strong Statement—Black Futures Turn Positive in Overnight Trading

Time:2025-10-28

-

Morning Read: China and the U.S. Reach Preliminary Consensus; Draft Opinions Sought on New Steel Capacity Replacement Plans

Time:2025-10-27

-

Morning Read: International commodity prices surged across the board, while supply and demand for the five major steel products both increased.

Time:2025-10-24

-

In the third quarter of 2025, Fortescue's iron ore production reached 50.8 million tons, representing a year-on-year increase of 6%.

Time:2025-10-23

-

Steel prices remain stagnant as the market awaits a breakthrough in macroeconomic conditions.

Time:2025-10-22

-

Morning Reading: China and the U.S. Agree to Hold a New Round of Economic and Trade Consultations; Steel Mills Reduce Production and Conduct Maintenance Inspections

Time:2025-10-20

-

Morning Reading: Sichuan's Steel Industry Advances Measures to Combat "Involution," While Several Steel Mills in Northern China Undertake Maintenance Overhauls.

Time:2025-10-16

-

Morning Reading: China Responds to U.S. Threat of Additional Tariffs on China, October North-to-South Steel Material Survey

Time:2025-10-13

-

Morning Reading: Two Departments Take Action to Address Unregulated Price Competition, Black Commodity Futures Turn Positive in Overnight Trading

Time:2025-10-10

-

Morning Reading: Steel inventories surged by 1.28 million tons during the holiday period; summary of performance for black commodity sectors

Time:2025-10-09

-

Morning reading: The State-owned Assets Supervision and Administration Commission urges central enterprises to take the lead in "fighting internal involution," as rebar prices fall below 3,100.

Time:2025-09-28

-

Morning Reading: Ministry of Commerce Counterattacks Mexico's China-Related Measures; Supply and Demand Both Rise for Five Major Steel Products

Time:2025-09-26

-

After the National Day holiday, the price of hot-rolled strip steel in China may rise first and then decline

Time:2025-09-25

-

South Korea's K-Steel bill is impacting our country's steel exports, and the three major coal import ports will shut down.

Time:2025-09-24

-

Black Metal Regular Meeting: This week, the steel market showed mixed trends, while raw materials may remain relatively strong.

Time:2025-09-23

-

Midday Report: Steel prices mainly rose, with coking coal futures climbing more than 5%.

Time:2025-09-16

-

A Brief Analysis of Profit Contraction Pressure on Domestic Tinplate Manufacturers

Time:2025-09-15

-

Afternoon Report: Localized Steel Price Increase, Iron Ore Futures Drop Over 1%

Time:2025-09-11

-

Morning reading: Latest survey on steel mill maintenance impact, structural steel production capacity adjustment enters a stable period

Time:2025-09-08

-

Morning reading: Tangshan Steel Plant resumes production in batches, Trump signs US-Japan trade agreement

Time:2025-09-05

-

Morning reading: Black futures declined in the night session, construction sites in Beijing-Tianjin-Hebei gradually resume work

Time:2025-09-04

-

The Breakthrough Path for Steel Enterprises under the Transformation and Upgrading of the Construction Industry

Time:2025-09-03

-

The steel market still has room to decline in September

Time:2025-09-02

-

Anti-dumping situation of foreign steel products against China from January to August

Time:2025-09-01

-

The European Union plans to eliminate tariffs on American industrial goods to alleviate the impact of car tariffs.

Time:2025-08-29

-

Reference | Interpretation of the second half market based on silicon steel supply and demand

Time:2025-08-28

-

WEEKLY SUMMARY: China's steel market slides on weak fundamentals

Time:2025-08-25

-

WEEKLY: Chinese mills' steel stocks edge down

Time:2025-08-22

-

Việt Nam imposes anti-dumping duties on Chinese and South Korean coated steel

Time:2025-08-19

-

Vietnam imposes AD duties on galvanized steel from China, South Korea

Time:2025-08-19

-

Detailed explanation of color-coated steel sheet types, colors, and applications

Time:2025-02-27

-

What is cold-rolled sheet material? A comprehensive analysis of the characteristics and applications of cold-rolled sheet.

Time:2025-01-08

-

Advantages and Applications of Cold-Rolled Sheet

Time:2025-01-08

-

Applications and characteristics of color-coated steel sheets

Time:2025-01-08

-

Detailed explanation of the function and advantages of color-coated steel plate

Time:2025-01-08

-

What thickness and width of stainless steel do you require?

Time:2025-01-08

Contact us for better prices!

Share your needs with us and get impressive cooperation and reliable products.